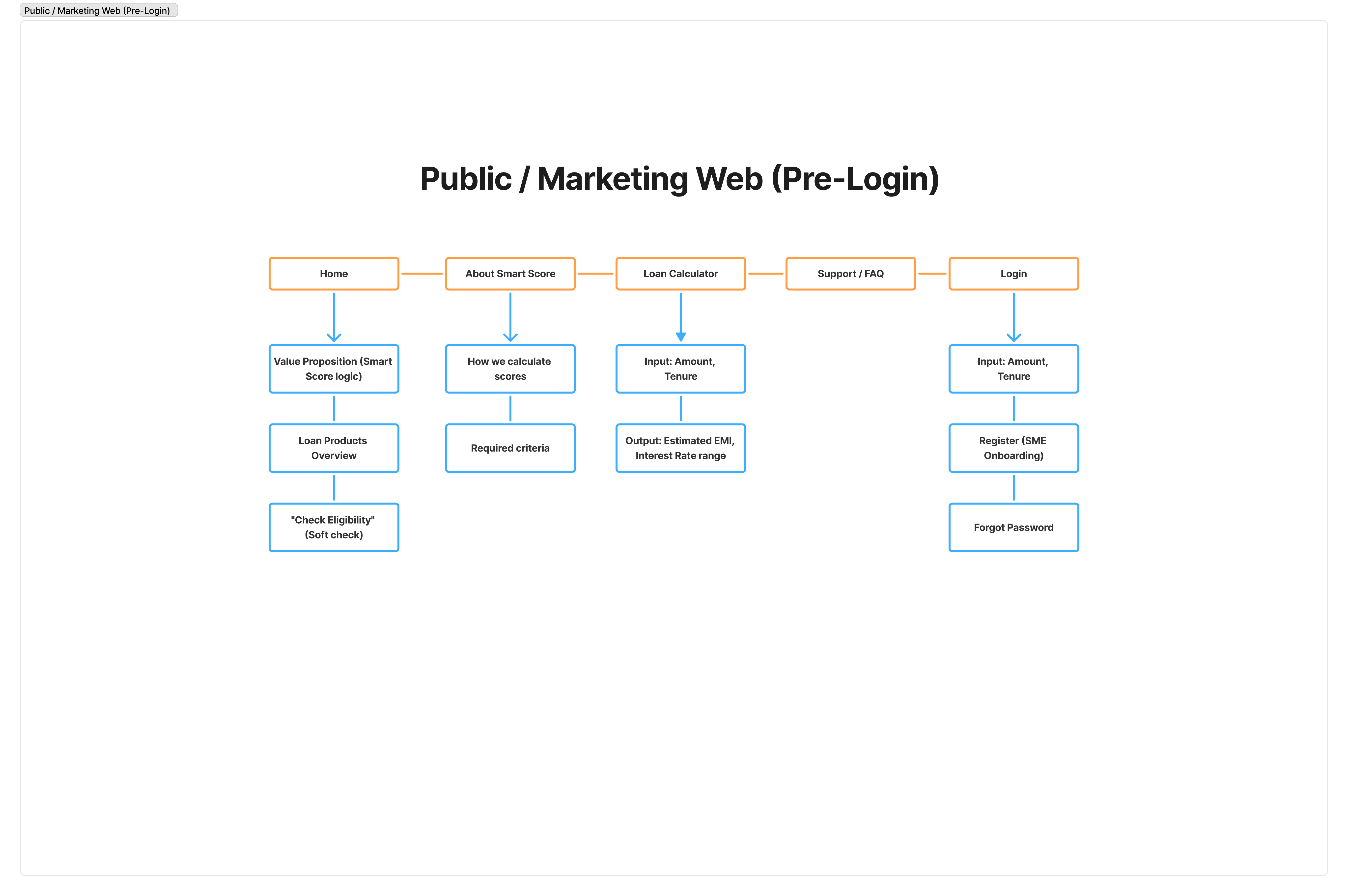

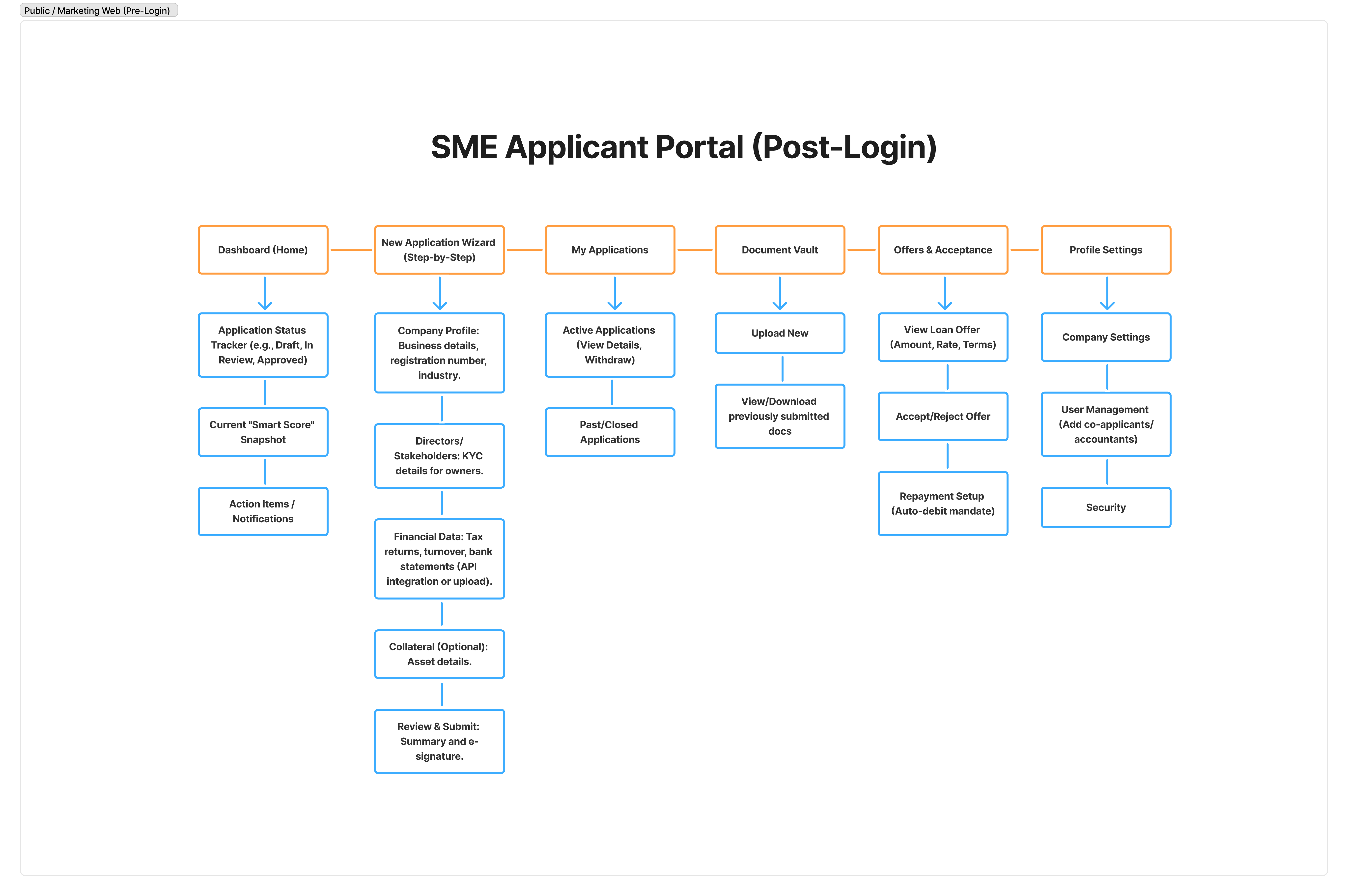

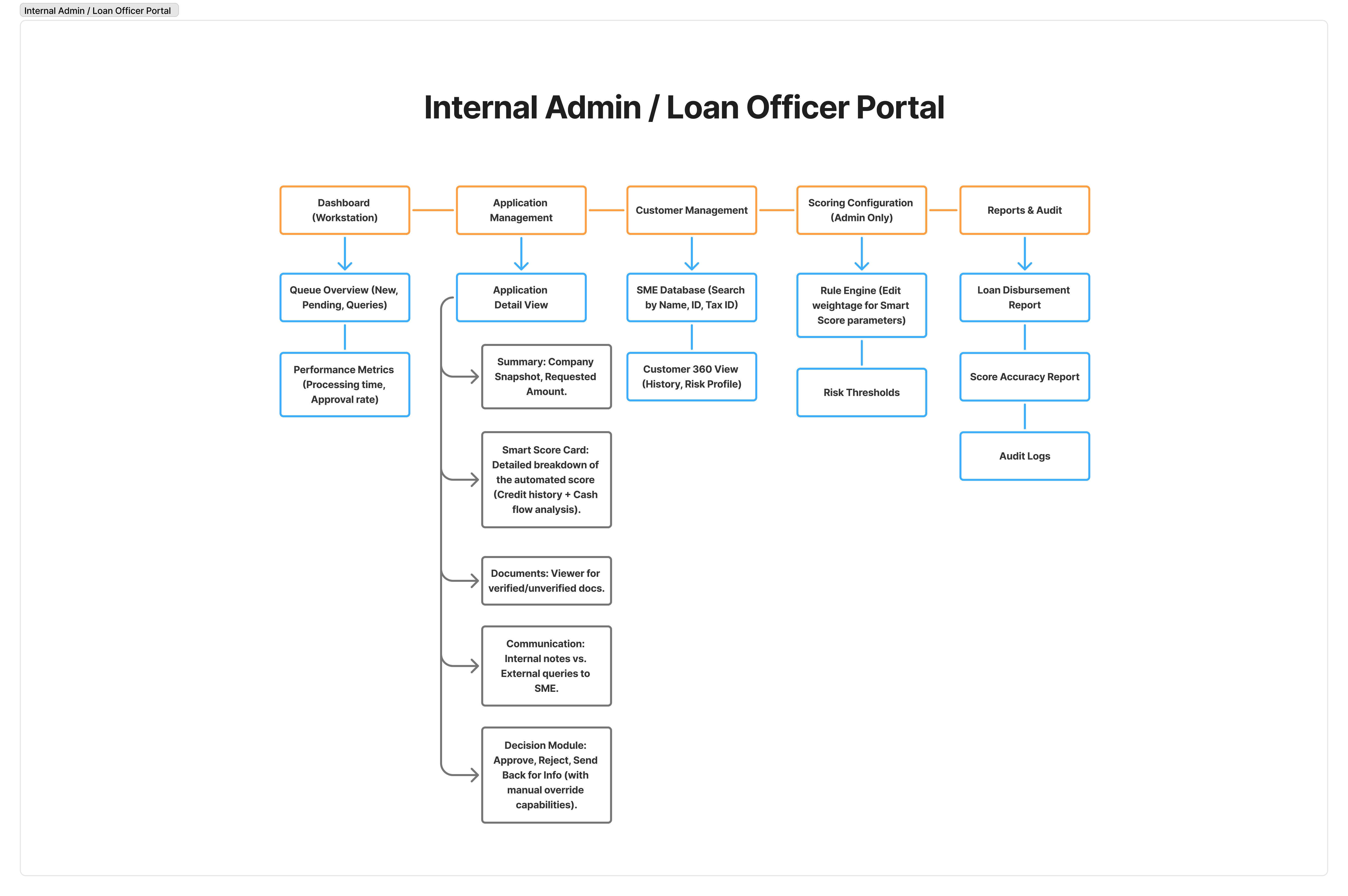

Here is a comprehensive Information Architecture (IA) for the SME Smart Score Loan Application Management System.

This structure is designed to support two distinct user journeys: the SME Applicant (seeking a loan) and the Bank/Loan Officer (processing the application and managing the “Smart Score”).

User Roles & Access Levels:

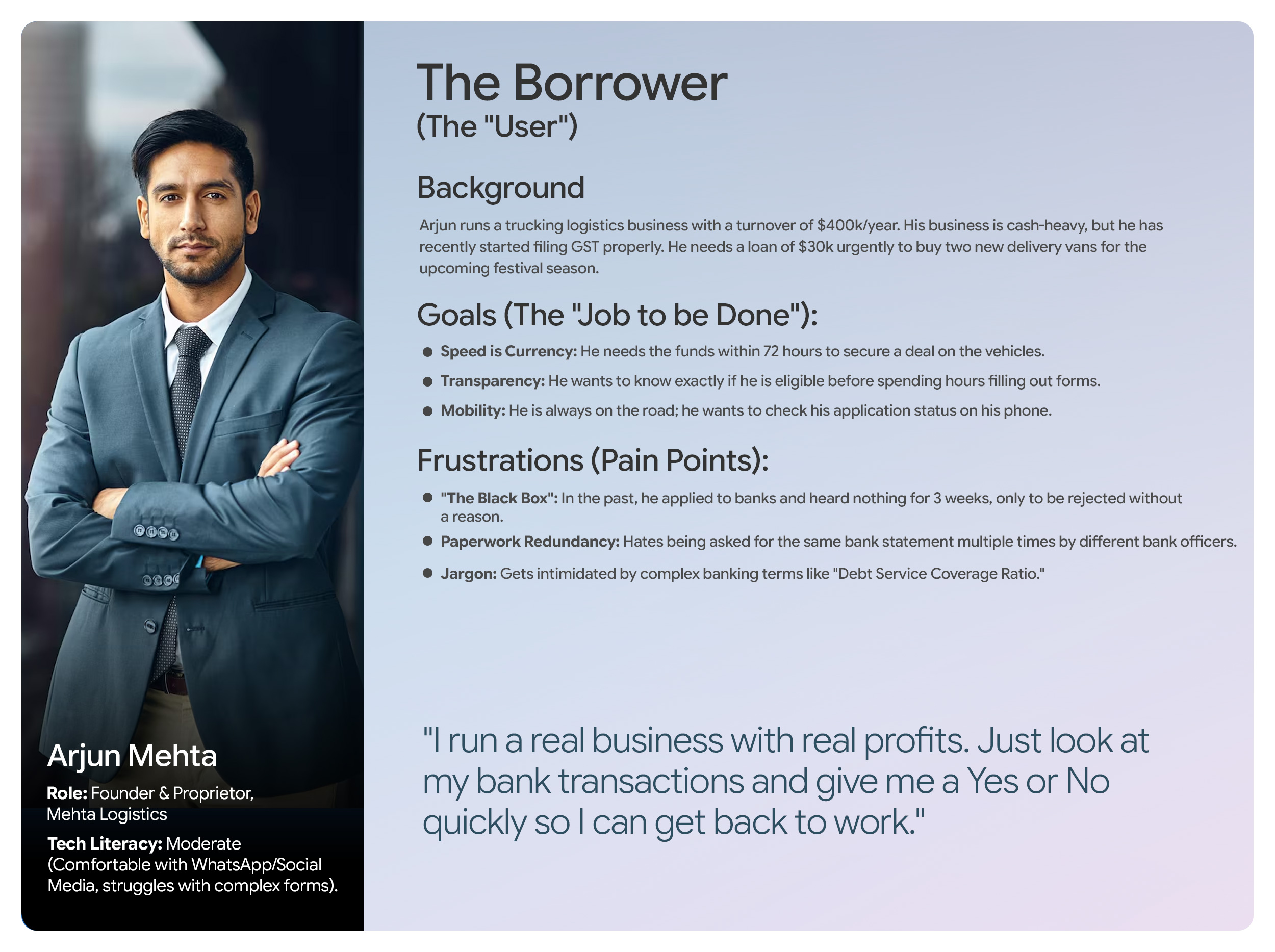

- Public User: Unregistered SME owner exploring options.

- SME Applicant: Registered user applying for a loan and tracking status.

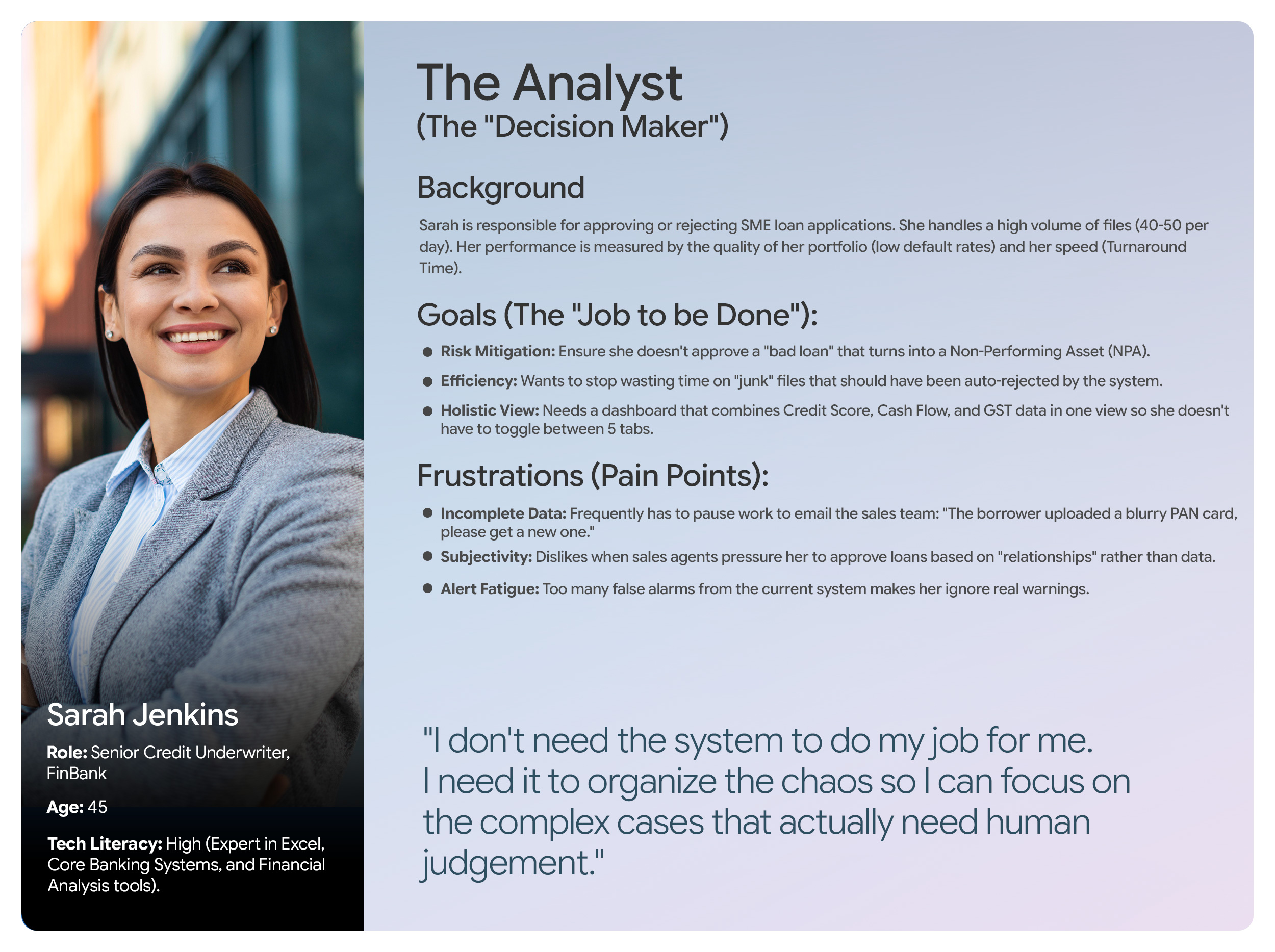

- Loan Officer / Underwriter: Internal staff reviewing applications and scores.

- System Admin: Manages configurations, scoring algorithms, and user access.